SIP Calculator: Plan Your Mutual Fund Investments

What Is a SIP?

A Systematic Investment Plan (SIP) is a method of investing in mutual funds where you invest a fixed amount at regular intervals — typically monthly — rather than investing a lump sum all at once.

Think of it like a recurring deposit, but instead of a fixed bank interest rate, your money goes into a mutual fund that invests in equities, debt, or a mix. The returns aren't guaranteed, but historically, equity mutual funds have significantly outperformed standard savings accounts over long periods.

SIPs are popular in India and South/Southeast Asia, where mutual fund investing has been made accessible through simple monthly auto-debit systems. But the underlying concept applies to any regular investment in any market globally.

How SIP Returns Work: The Power of Compounding

The math behind SIP growth involves compound interest on periodic contributions. Unlike a one-time investment, each monthly instalment has a different time horizon — the first month's payment compounds for the entire duration, the last month's payment barely compounds at all.

The formula for SIP return:

FV = P × [((1 + r)^n − 1) ÷ r] × (1 + r)

Where:

FV = Future Value

P = Monthly investment amount

r = Monthly rate of return (annual rate ÷ 12)

n = Number of months

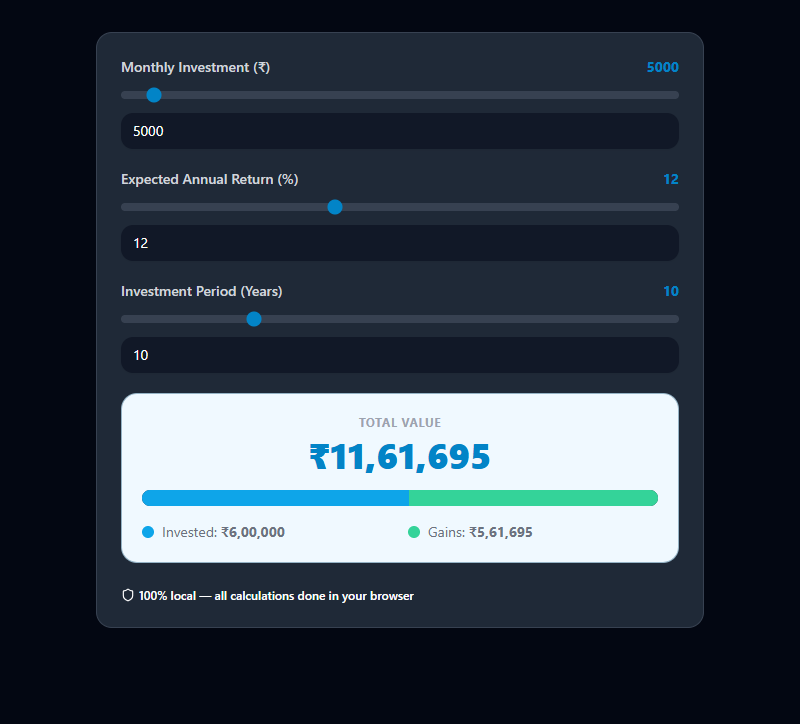

Example:

- Monthly SIP: ₹5,000

- Expected annual return: 12%

- Duration: 10 years (120 months)

Monthly rate r = 12% ÷ 12 = 1% = 0.01

FV = 5000 × [((1.01)^120 − 1) ÷ 0.01] × 1.01

FV ≈ ₹11,61,695

Total invested: ₹5,000 × 120 = ₹6,00,000 Returns generated: ₹5,61,695 Wealth created through compounding: ₹5.6 lakh on a ₹6 lakh investment

What Return Rate Should You Use?

Expected return rates for different fund categories (based on long-term Indian market historical data):

| Fund Type | Expected Annual Return | Risk Level |

|---|---|---|

| Liquid / Money Market | 5–6% | Very Low |

| Debt / Fixed Income | 7–9% | Low |

| Hybrid / Balanced | 10–12% | Medium |

| Large Cap Equity | 12–14% | Medium-High |

| Mid Cap Equity | 15–18% | High |

| Small Cap Equity | 18–22% | Very High |

| Index Fund (Nifty 50) | 12–14% | Medium |

Important: These are historical averages, not guarantees. Markets go through periods of poor performance. The longer your investment horizon, the more these averages tend to hold. For goals shorter than 5 years, equity funds carry significant risk of underperformance.

For calculation purposes, most financial planners use 12% for equity SIPs as a conservative long-term estimate.

SIP vs. Lump Sum: Which Is Better?

Both have their place, and they're not mutually exclusive:

SIP advantages:

- Rupee cost averaging — When markets fall, your fixed monthly amount buys more units. When markets rise, you buy fewer. Over time, this averages out your purchase cost.

- Discipline — Automating a monthly investment removes the temptation to spend.

- No need to time the market — You don't need to figure out the "right" time to invest.

- Lower entry barrier — Start with as little as ₹500/month.

Lump sum advantages:

- Better returns if you invest at a market low.

- Simple — one decision, one transfer.

- The entire amount starts compounding from day one.

In practice: SIP for regular income investors; lump sum when you have a windfall and a long investment horizon. Many investors do both — a regular SIP plus a lump sum top-up when they receive bonuses or windfalls.

Setting a Realistic SIP Goal

Working backwards from a goal using our calculator:

Goal: Accumulate ₹1 crore in 15 years at 12% CAGR.

The calculator tells you: You need to invest approximately ₹20,000 per month.

If that's too much, you can adjust:

- Extend the timeline to 20 years → reduces required SIP to ~₹10,000/month

- Accept a higher-risk fund targeting 15% → reduces required SIP to ~₹14,500/month

- Combine SIP with a lump sum starting amount

Step-up SIP: Many fund houses allow step-up (or top-up) SIPs, where you increase the contribution by a fixed percentage each year (aligned with salary increases). Our calculator supports step-up modeling — increasing your SIP by even 10% annually dramatically improves the outcome.

Common SIP Mistakes to Avoid

Stopping during market downturns. When your portfolio is down 20%, it feels wrong to keep investing. But those are exactly the months where your SIP buys the most units at cheap prices. Stopping a SIP during a crash locks in losses and removes future upside.

Too many funds. Diversification is good. Owning 15 different equity mutual funds is not diversification — it's confusion. 3–4 well-chosen funds covering different categories provide adequate diversification without overlap.

Checking portfolio value too often. Short-term volatility is noise. An equity SIP should be evaluated on its 5–10 year trajectory, not daily or monthly.

Not factoring inflation. A future value of ₹1 crore in 20 years has significantly less purchasing power than ₹1 crore today. Always calculate your target in today's rupee value and then adjust for expected inflation.